One of the biggest misconceptions about the VA loan is that it is a one time benefit. That is flat out wrong. And that misunderstanding alone costs veterans thousands in lost opportunity.

You can use your VA loan more than once. You can have more than one VA loan at the same time. And if you are active duty, your PCS moves can become one of the best wealth building strategies available to you.

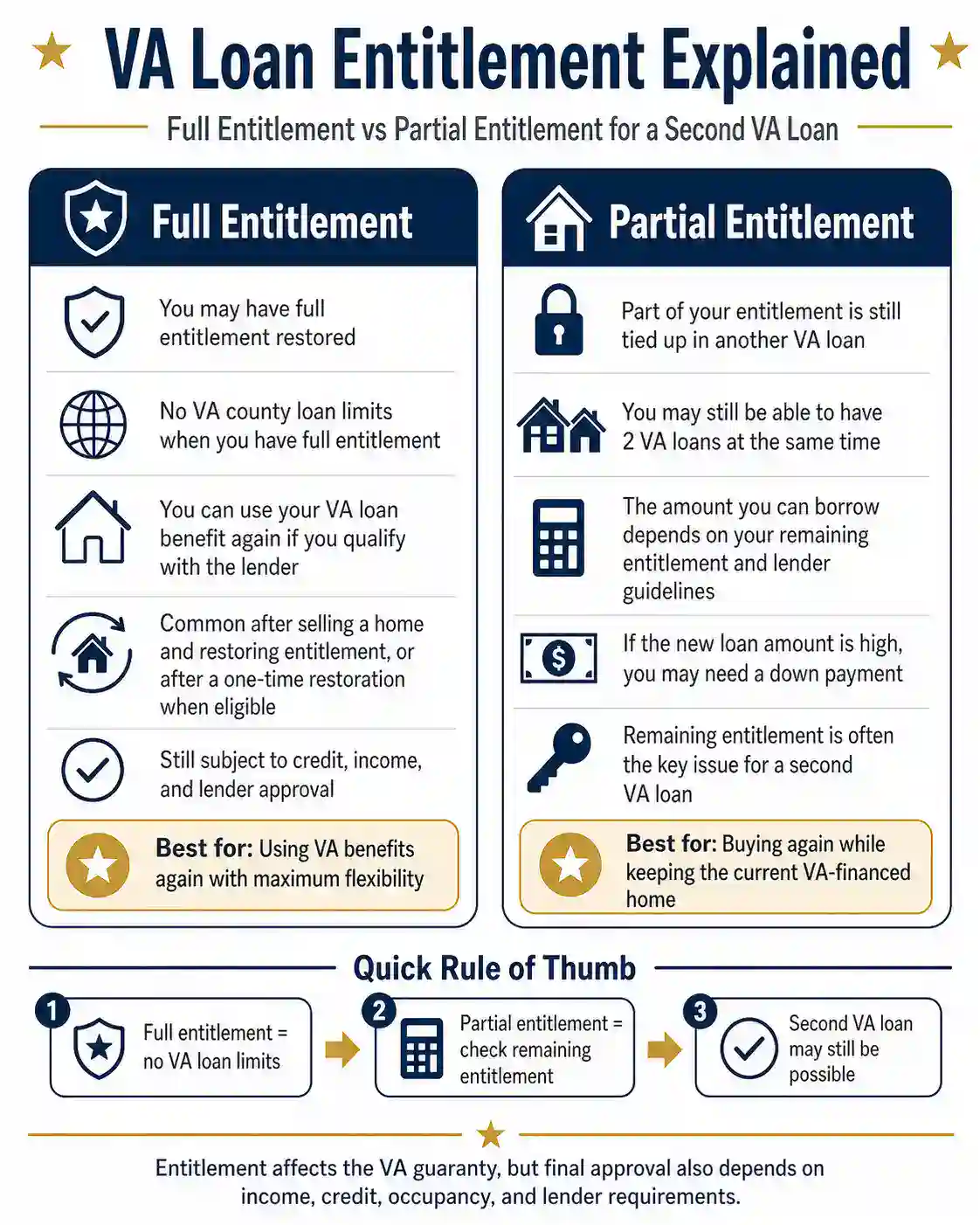

How VA Loan Entitlement Actually Works

Your VA loan entitlement is the amount the VA will guarantee on your behalf. It determines how much you can borrow without a down payment.

If you have full entitlement, meaning you have never used a VA loan, have used one and sold the property with the loan fully paid, or have had your entitlement restored, there is no loan limit. You can borrow as much as a lender will approve you for based on your income and credit.

If you have partial entitlement, meaning you currently have one VA loan active, the county loan limit comes into play. You will have residual entitlement left over. That residual entitlement equates to a certain purchase price that you can buy at zero down. Anything above that amount requires 25% down on the difference.

It sounds complicated, but it is very manageable once you understand your numbers. Our VA Loan Entitlement Calculator walks you through exactly how much entitlement you have remaining and what that means for your next purchase.

Turning PCS Moves Into a Portfolio

Here is the strategy in simple terms.

You buy at your first duty station using your VA loan. When you PCS, instead of selling, you keep that home as a rental. Then you buy again at your next duty station, either with your remaining VA entitlement or by refinancing the first home into a conventional loan and restoring your full entitlement through a one time restoration.

That is two properties. Both building equity. Both appreciating. One generating rental income while you live in the other.

Do it again at your third duty station and now you have three.

My wife and I followed a version of this path. We bought our first home in San Diego in 2007. It was a condo. Not what we wanted, not where we wanted, but it was what we could afford and it made sense at the time. Nine years later, we sold and used that equity to buy a single family home. That home eventually became a rental when our family situation changed. Then we added another rental, this time with a conventional loan and 20% down.

It was not fast. It was not glamorous. But it was consistent. And each step created options for the next.

Buy Like You Might Become a Landlord

The key to making this work is buying with a plan. If there is a chance you will rent the property when you leave, you need to be thinking like a landlord on day one.

That means paying attention to things most first time buyers ignore. What does rent look like in the area? Is the home in a location that attracts tenants, whether that is young military families, single service members, or civilian renters? Are the schools rated well? Is it close to base?

You do not need to have kids to care about schools. School ratings directly impact property values and the quality of tenants your home will attract.

Also think about size and layout. Buying a 6,000 square foot dream home when it is just you and your spouse might feel great, but if you PCS in two years and cannot rent it for enough to cover the mortgage, you are stuck. Buy something closer to what the local rental market supports. If you would have been renting a two or three bedroom apartment, buy the equivalent. Your BAH goes further, and the home is easier to rent later.

Wondering what your BAH and income can actually support? Our VA Loan Buying Power Calculator can help you see what price range makes sense before you start shopping.

What to Watch Out For

A few things can derail this strategy if you are not careful.

First, understand what happens if you cannot sell. When you put zero down and only own the home for a year or two, there may not be enough appreciation to cover the cost of a sale, including commissions, title, and escrow fees. If that is the case, renting becomes the move. But you need to know in advance whether the rental income will cover the mortgage or if there is a gap you will need to fund out of pocket.

Second, do not assume rent will equal your mortgage payment. In a lot of markets, especially high cost ones, there can be a gap. That is okay if you plan for it. It is not okay if it surprises you.

Third, if you end up in a position where you cannot sell and cannot afford to rent it at a loss, the options get limited. Short sales and foreclosures can hurt your credit and impact your ability to use the VA loan in the future. Planning ahead prevents that.

The Bigger Picture

This is not about buying as many houses as possible. It is about being intentional with a benefit that most people underuse.

Every PCS does not have to be a purchase. But every PCS should include the conversation. What are the numbers? Does it make sense? What does the rental market look like? What are the tax implications if I keep it or sell it?

Having a good team, a realtor who knows the local market and a lender who understands VA entitlement, makes those conversations productive instead of overwhelming.

The VA loan is not a one time tool. It is a renewable benefit that, when used strategically, can help you build a portfolio of properties over the course of a military career. Most people just do not know that. Now you do.

Jason Rivera is a Navy veteran and co-owner of Legacy Realty Network, a veteran-owned company serving San Diego County. He is also a licensed Realtor and Mortgage Loan Officer (NMLS #2562702), handling both the real estate and the mortgage in-house so your transaction never gets handed off mid-process. If you’re ready to put your VA benefit to work, reach out to our team today.